Policy Learning with the polle package

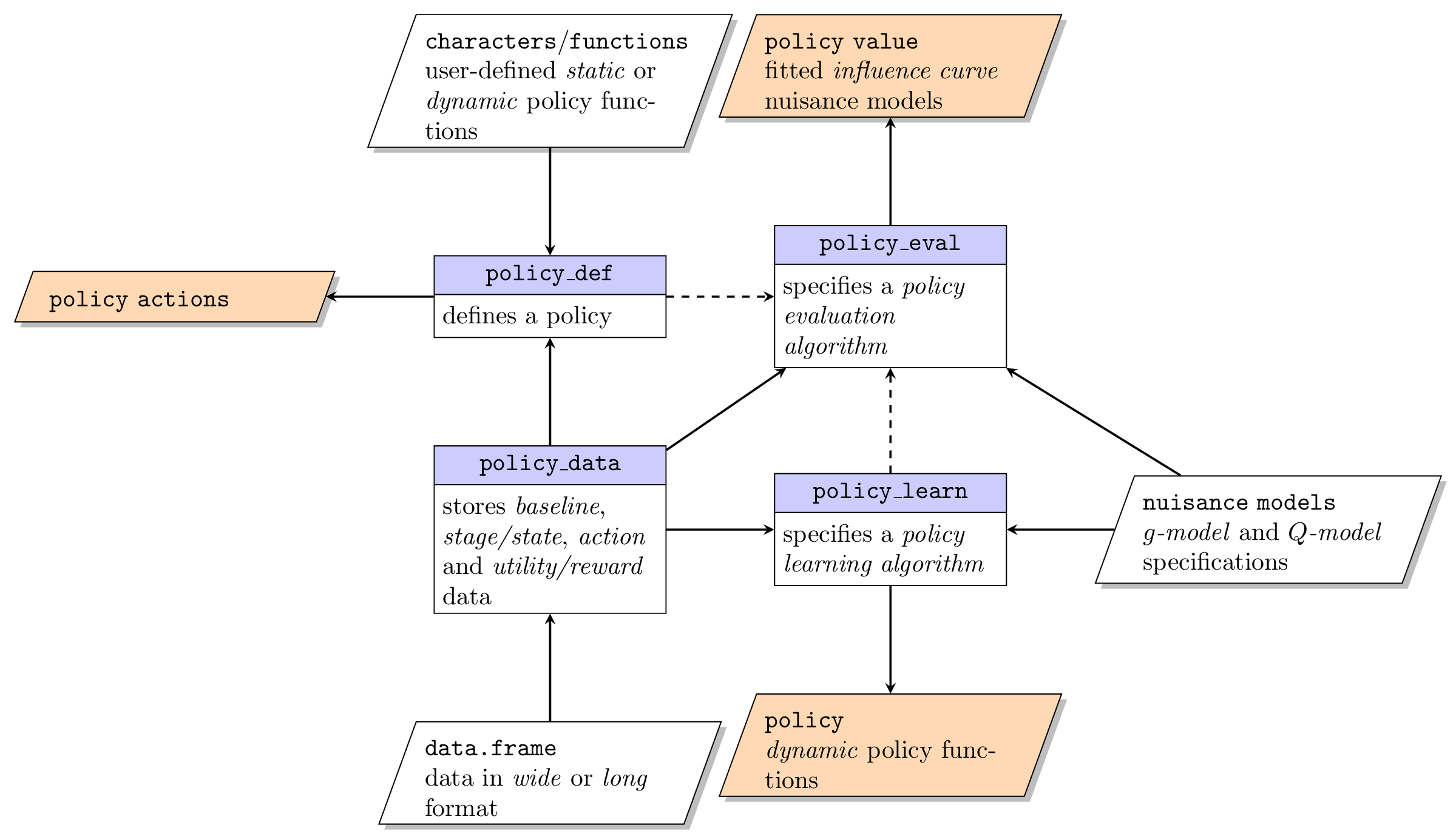

The R package polle is a unifying framework for learning and evaluating finite stage policies based on observational data. The package implements a collection of existing and novel methods for causal policy learning including doubly robust restricted Q-learning, policy tree learning, and outcome weighted learning. The package deals with (near) positivity violations by only considering realistic policies. Highly flexible machine learning methods can be used to estimate the nuisance components and valid inference for the policy value is ensured via cross-fitting. The library is built up around a simple syntax with four main functions policy_data(), policy_def(), policy_learn(), and policy_eval() used to specify the data structure, define user-specified policies, specify policy learning methods and evaluate (learned) policies. The functionality of the package is illustrated via extensive reproducible examples.